From April to May 2026, global biopharma dealmaking showed a clear rebound. Large pharmaceutical companies continued to strengthen their pipelines through acquisitions, Chinese innovative drug assets maintained strong outbound licensing momentum, and platform technologies such as ADCs, TCEs, multispecific antibodies, siRNA, AI drug discovery, cell therapy, and radiopharmaceuticals became key areas of capital and business development activity.

Overall, the main themes of the past two months can be summarized as: big pharma acquiring high-certainty assets, Chinese biotech companies exporting innovation, and next-generation platform technologies gaining higher strategic value.

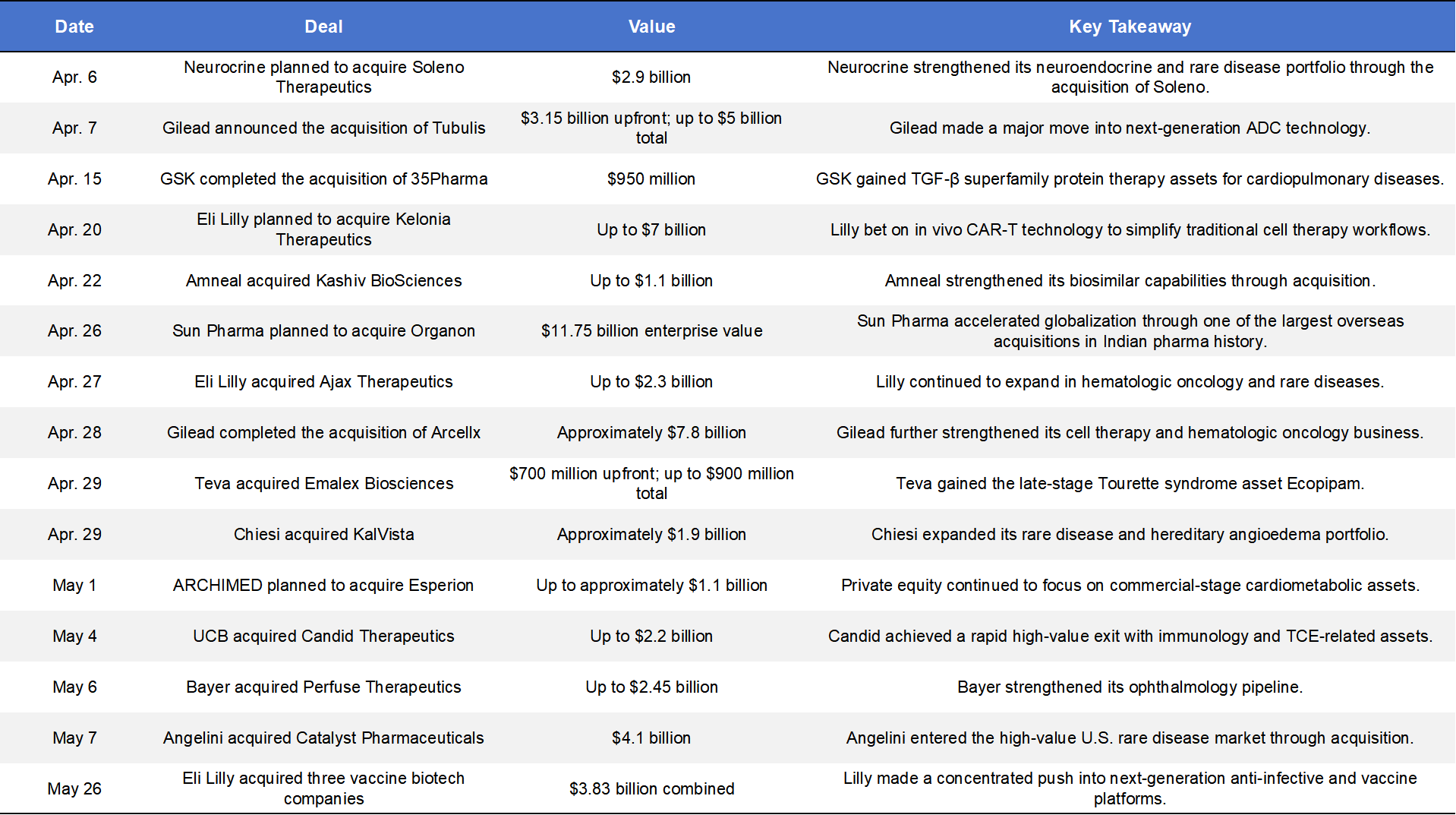

1. Large-Scale M&A Rebounds: Big Pharma Moves Quickly to Strengthen Core Therapeutic Areas

From April to May, multiple billion-dollar acquisitions were announced or completed. These deals show that global pharmaceutical companies are using external transactions to fill internal pipeline gaps, with a focus on oncology, rare diseases, ophthalmology, immunology, cardiovascular disease, and cell therapy.

Big pharma’s acquisition strategy has shifted from broad exploration to buying high-certainty assets. Programs with clinical validation, differentiated mechanisms, commercial potential, or platform scalability continue to command premium valuations.

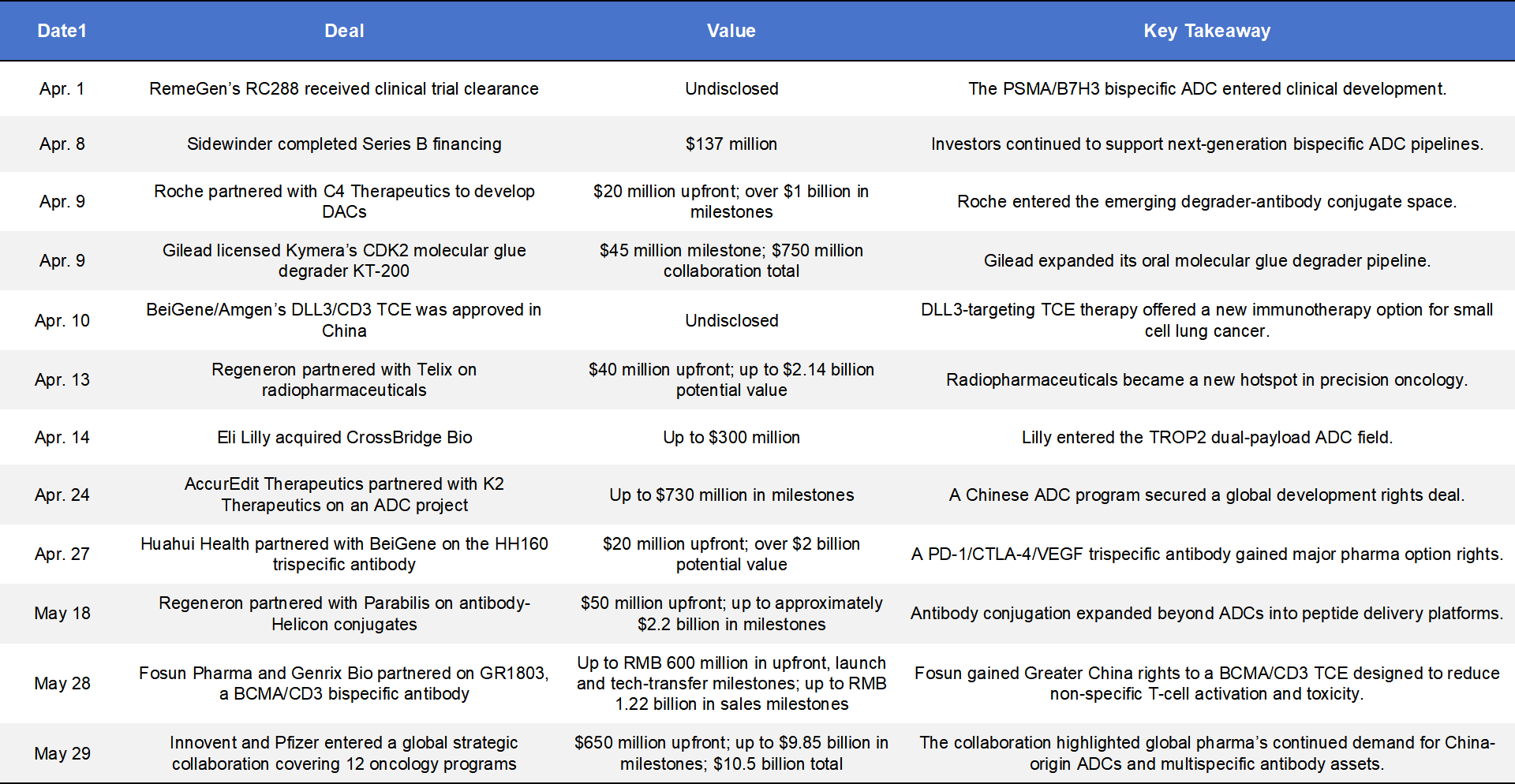

2. Oncology Remains the Core Dealmaking Field: ADCs, TCEs, Multispecific Antibodies, and Conjugation Platforms Stay Hot

Oncology remained the most active therapeutic area. ADCs are moving beyond traditional single-payload formats toward dual-payload ADCs, bispecific ADCs, degrader-antibody conjugates, and antibody-peptide conjugates. TCEs, multispecific antibodies, and radiopharmaceuticals also attracted strong interest from major pharma companies.

Oncology dealmaking is evolving from single-target competition to a “platform technology plus multi-mechanism combination” model. ADCs, DACs, multispecific antibodies, TCEs, and radiopharmaceuticals are together shaping the next generation of precision cancer therapy. The latest Innovent-Pfizer and Fosun-Genrix deals further confirm that China-origin oncology platforms are becoming an increasingly important source of global innovation.

3. Chinese Innovative Drug BD Remains Active: From Single-Asset Licensing to Portfolio-Based and Platform-Driven Global Deals

Chinese biopharma companies were highly active in April and May, with deal structures becoming increasingly sophisticated. Transactions are no longer limited to single-product regional licensing; they now include multi-asset collaborations, global options, commercialization rights, and NewCo models.

Chinese innovative drug out-licensing is moving from single-product BD to a new phase of portfolio licensing, platform value recognition, and global development collaboration. Deals involving Hengrui, Innovent, RemeGen, Ribo, CSPC/Jushi Bio and Haisco show that Chinese biotech companies are gaining stronger global negotiation power, especially in ADCs, multispecific antibodies, siRNA, peptide platforms and long-acting delivery technologies.

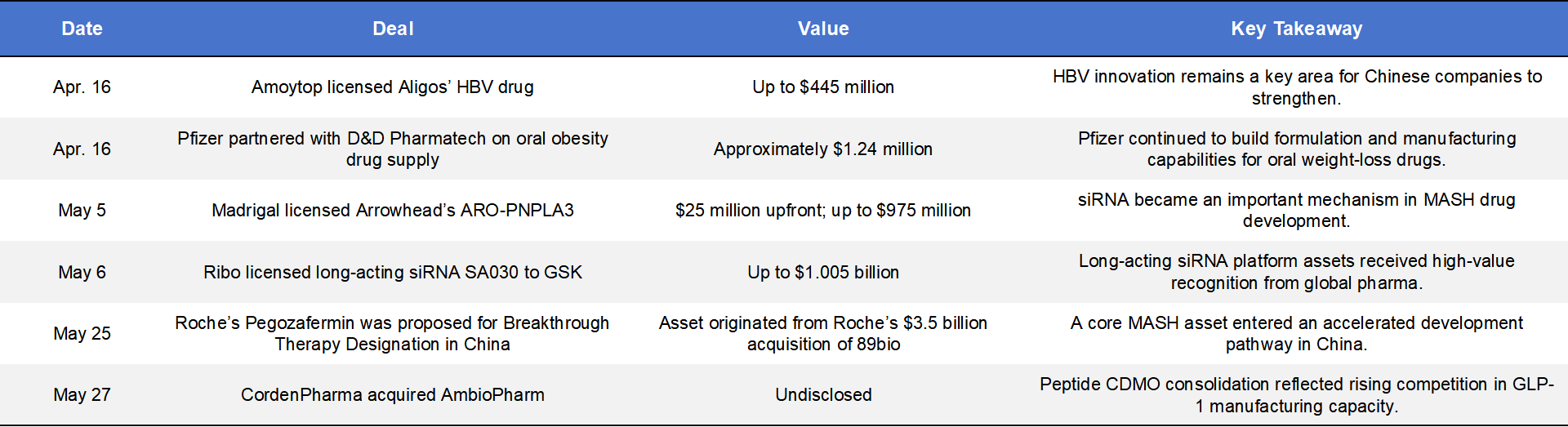

4. RNA Drugs, Metabolic Diseases, and the GLP-1 Supply Chain Continue to Heat Up

RNA therapeutics, MASH, HBV, obesity, and the GLP-1 supply chain were important non-oncology hotspots in April and May. Transactions occurred not only around drug assets, but also around formulation, CDMO capacity, and peptide manufacturing.

The deal logic in metabolic disease and RNA therapeutics is becoming clearer: big pharma buys mechanisms, biotech companies export platforms, and CDMOs compete for manufacturing capacity. MASH, HBV, GLP-1, and siRNA will likely remain important BD themes.

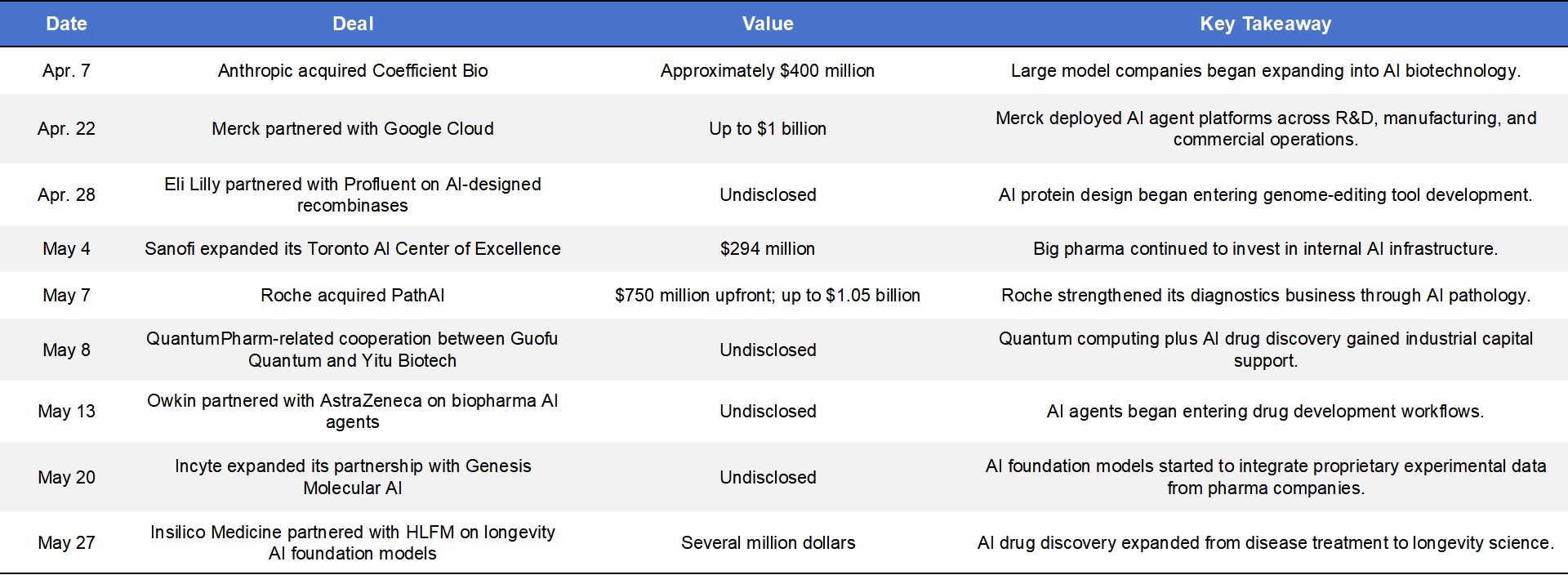

5. AI Drug Discovery Moves from Concept Validation to Industrial-Scale Collaboration

AI-related deals increased significantly in April and May. These collaborations are no longer limited to early-stage discovery, but now span R&D, diagnostics, manufacturing, commercialization, and foundation model development.

AI drug discovery is moving from “model storytelling” to industrial implementation. Companies that control high-quality experimental data, validated models, and concrete application scenarios will hold greater commercial value.

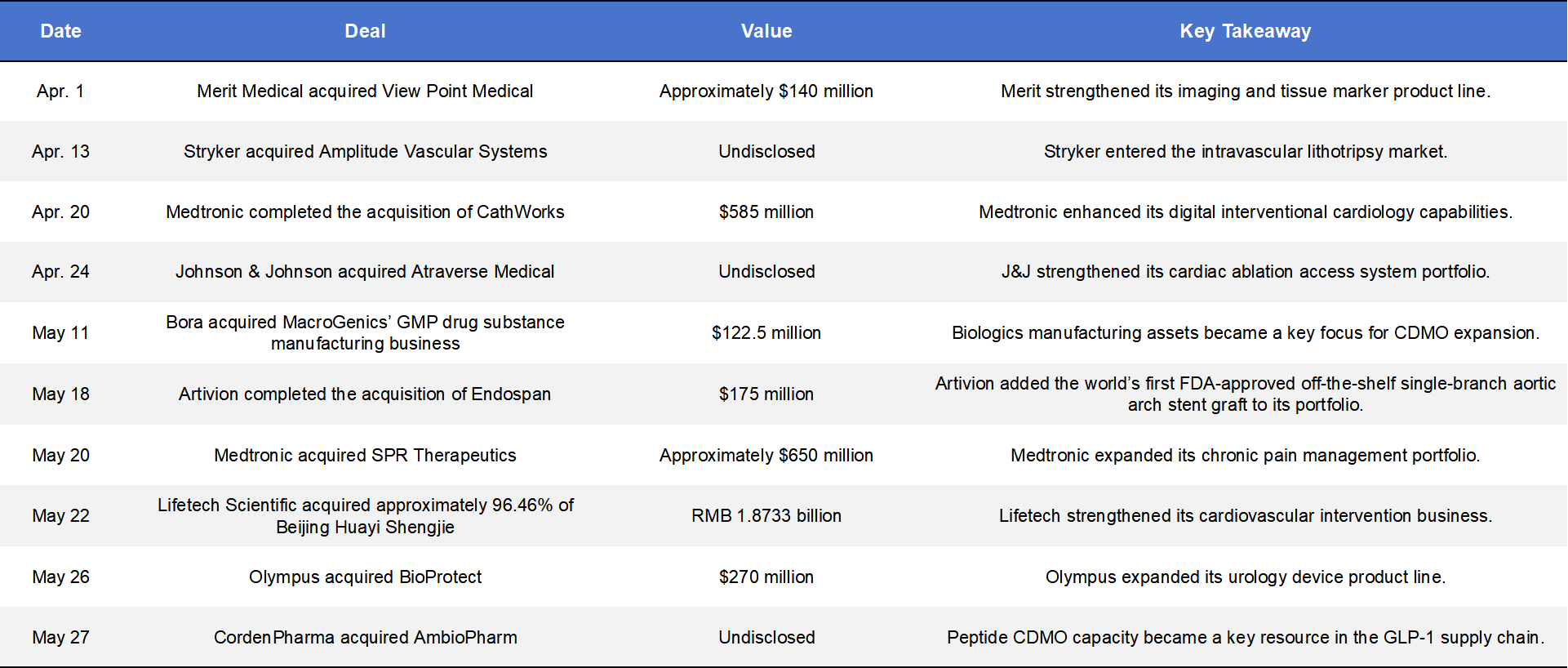

6. Medical Device and CDMO Consolidation Accelerates: Manufacturing Capability Becomes a Strategic Asset

Medical device and manufacturing-related transactions were also active. Large device companies acquired assets to strengthen niche segments, while CDMO companies expanded capacity around biologics, peptides, and complex formulations.

Medical device deals focused on strengthening niche segments, while CDMO deals highlighted the strategic value of complex drug manufacturing. Artivion’s acquisition of Endospan further shows that differentiated, regulatory-approved cardiovascular devices remain attractive strategic assets for global medtech leaders.

7. Domestic Asset Restructuring Remains Active as Chinese Pharma Companies Refocus on Core Businesses

In China, multiple equity transfers and asset restructuring deals showed that pharmaceutical companies are accelerating portfolio adjustments. Some listed companies are seeking a second growth curve through pharma assets, while biotech companies are selling assets to ease commercialization pressure and improve cash flow.

Overall, the April–May 2026 deal landscape shows that biopharma transactions are entering a more selective but high-value phase. Mega deals such as the $15.2B Hengrui–BMS partnership, the $10.5B Innovent–Pfizer collaboration, and CSPC/Jushi Bio’s $420M upfront payment from AstraZeneca highlight the rising global value of China-origin innovation. At the same time, large pharma companies are prioritizing clinically validated assets, differentiated mechanisms, and scalable platforms across ADCs, multispecific antibodies, siRNA, AI-enabled drug discovery, and advanced delivery technologies. The next cycle of biopharma BD will likely be driven by asset quality, platform depth, and global execution capability.